Hello Friends! Are you looking to invest in the stock market, or have you already invested? Would you like to know the predictions regarding the potential fluctuations in your shares? If so, you have landed on exactly the right page. On this page, you will find information regarding Jana Small Finance Bank share price, AU Small Finance Bank Loan details, Au small finance bank share price future, AU Small Finance Bank net worth, Au small finance bank share price history, and much more. Furthermore, this page provides details on AU Small Finance Bank‘s share price targets 2026, 2027, 2028, 2029, 2030, 2040, and beyond.

AU Small Finance Bank Company Information

| Industry | Banking Financial services |

| Founded | 1996; 30 years ago |

| Founder | Sanjay Agarwal |

| Headquarters | Jaipur, Rajasthan, India (registered office) BKC, Mumbai, India (corporate office) |

| Key people | H R Khan (Chairman) Sanjay Agarwal (MD & CEO) |

AU Small Finance Bank Share Price Target Overview

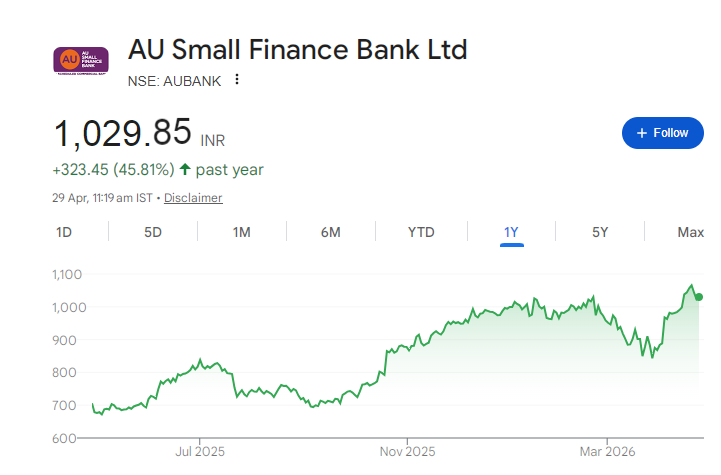

- Current Price – 1,029.75

- Open – 1,030.50

- High – 1,037.20

- Low – 1,019.55

- Mkt cap – 77.10KCr

- P/E ratio – 33.28

- 52-wk high – 1,079.55

- 52-wk low – 655.50

- Dividend – 0.097%

- Qtrly div amt – 0.250

AU Small Finance Bank Share Price Chart

AU Small Finance Bank Share Price Target Tomorrow

| AU Small Finance Bank Share Price Target Years | AU Small Finance Bank Share Price Target |

| 2026 | ₹1100 |

| 2027 | ₹1400 |

| 2028 | ₹1700 |

| 2029 | ₹2000 |

| 2030 | ₹2300 |

AU Small Finance Bank Share Price Target 2026

The target for AU Small Finance Bank’s share price in 2026 is projected to range between ₹1070 and ₹1100. As of the end of April 2026, AU Small Finance Bank’s share price stood at ₹1,029.75. Compared to the previous year, AU Small Finance Bank’s share price has witnessed an increase this year.

AU Small Finance Bank Share Price Target 2027

The target for AU Small Finance Bank’s share price in 2027 is projected to range between ₹1380 and ₹1400. On 29 April 2026, AU Small Finance Bank Share price NSE is 1,029.75 INR. Compared to last year, no significant difference has been observed in the share price of AU Small Finance Bank. The share price has increased by approximately 250-300 rupees.

AU Small Finance Bank Share Price Target 2030

The target for AU Small Finance Bank’s share price in 2030 is projected to range between ₹1280 and ₹2300. Over the past several years, the company has generated substantial profits, and investors, too, have earned handsome returns proportionate to their shareholdings. We remain optimistic that the company will continue to generate profits in the future, thereby ensuring continued returns for its investors.

Risks and Challenges Of AU Small Finance Bank Share Price

Here are 8 key factors affecting the growth of AU Small Finance Bank share price:

1. Rising NPAs & Asset Quality Stress – The bank has seen an increase in bad loans (GNPA), especially in unsecured segments like microfinance and credit cards. This raises risk for future earnings.

2. High Credit Cost Pressure – Due to rising defaults, the bank has to set aside more provisions. Higher credit cost reduces profitability and limits share price growth.

3. Margin Pressure (Falling NIM) – Net Interest Margin has declined due to:

- Rising cost of funds

- Competitive lending rates

This directly impacts profit growth.

4. Strong Competition from Big Banks & Fintech – Large banks like HDFC Bank and ICICI Bank, along with fintech lenders, are aggressively expanding. This puts pressure on growth and pricing power.

5. Risk from Unsecured Loan Portfolio – Exposure to unsecured loans (personal loans, credit cards, microfinance) increases risk because these loans are more sensitive during economic slowdown.

6. Dependence on Non-Core Income – At times, a large portion of profits comes from non-operating income, which is not stable and can create volatility in earnings.

7. Sector & Market Sentiment Risk – Small finance banks are more volatile. Negative sentiment in the banking or midcap sector can cause sharp fall in share price even if fundamentals are stable.

8. Regulatory & Transition Risk (Universal Bank Shift) – As the bank moves toward becoming a universal bank, it will face:

- Stricter regulations

- Higher compliance costs

- Need for more capital

Any delay or challenge can impact growth expectations.

Read Also:- Meghna Infracon Share Price Target Tomorrow From 2026 to 2030 – Current Chart, Market Overview

Key Factors Affecting Growth AU Small Finance Bank Share Price

Here are 8 key factors affecting the growth of AU Small Finance Bank share price:

1. Strong Loan Growth (Credit Expansion) – The bank’s ability to grow its loan book—especially in retail, MSME, and vehicle finance—directly boosts interest income and overall earnings.

2. Improvement in Asset Quality (Lower NPAs) – Reduction in bad loans improves profitability and builds investor confidence, which positively impacts the share price.

3. Net Interest Margin (NIM) Stability – Maintaining strong NIM is crucial. Higher spreads between lending and borrowing rates lead to better profitability.

4. Deposit Growth & CASA Ratio – Higher deposits, especially low-cost CASA deposits, reduce funding costs and improve margins—key for long-term growth.

5. Expansion into New Segments – Growth in new areas like:

- Credit cards

- Microfinance

- Digital lending

can diversify revenue and support faster expansion.

6. Transition to Universal Bank – The bank’s potential transition from a small finance bank to a universal bank can:

- Increase business opportunities

- Improve valuation

- Attract more investors

7. Digital Banking & Technology Adoption – Investment in digital platforms improves customer experience, reduces costs, and helps compete with larger private banks and fintech players.

8. Economic Growth & Financial Inclusion – As India’s economy grows and financial inclusion increases, demand for loans and banking services rises—benefiting AU Small Finance Bank.

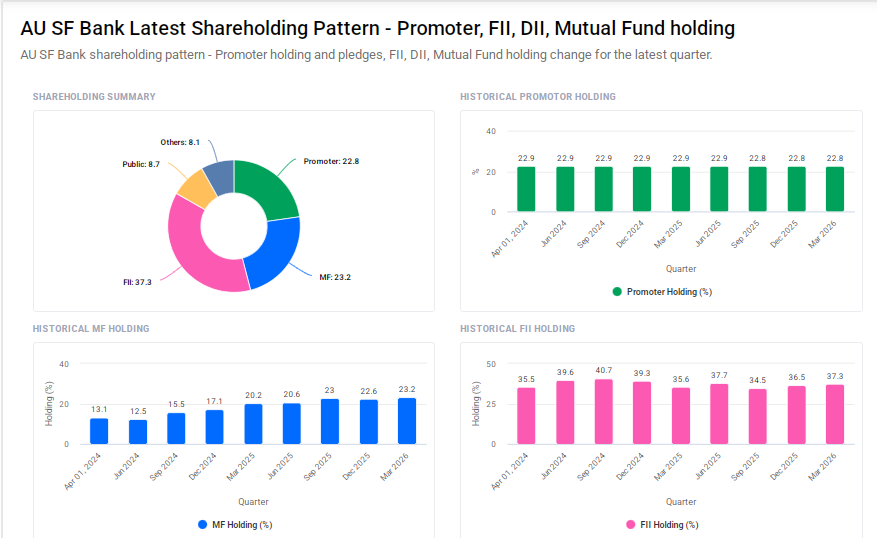

AU Small Finance Bank Shareholding Pattern

| Promoter | 22.8% |

| FII | 37.3% |

| DII | 31.3% |

| Public | 8.7% |

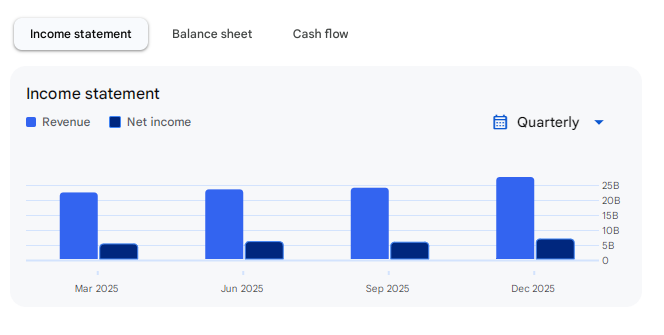

Income Statement Of AU Small Finance Bank

|

All values in INR

|

Mar 2025

|

Jun 2025

|

Sep 2025

|

Dec 2025

|

|---|---|---|---|---|

|

Revenue

|

22.19B

|

23.22B

|

23.76B

|

27.34B

|

|

Cost of goods sold

|

–

|

–

|

–

|

–

|

|

Cost of revenue

|

–

|

–

|

–

|

–

|

|

Research and development expenses

|

–

|

–

|

–

|

–

|

|

Total research and development expenses

|

–

|

–

|

–

|

–

|

|

Selling, general, and admin expenses

|

29.11B

|

8.66B

|

9.19B

|

10.19B

|

|

Operating expense

|

15.62B

|

15.43B

|

16.47B

|

18.50B

|

|

Total operating expenses

|

15.62B

|

15.43B

|

16.47B

|

18.50B

|

|

Operating income

|

6.57B

|

7.79B

|

7.29B

|

8.84B

|

|

Other non operating income

|

–

|

–

|

–

|

–

|

|

EBT including unusual items

|

6.57B

|

7.79B

|

7.29B

|

8.84B

|

|

EBT excluding unusual items

|

6.57B

|

7.79B

|

7.29B

|

8.84B

|

|

Income tax expense

|

1.53B

|

1.98B

|

1.68B

|

2.17B

|

|

Effective tax rate

|

23.35%

|

25.43%

|

23.05%

|

24.49%

|

|

Other operating expenses

|

-14.06B

|

6.78B

|

7.29B

|

8.31B

|

|

Net income

|

5.04B

|

5.81B

|

5.61B

|

6.68B

|

|

Net profit margin

|

22.69%

|

25.02%

|

23.60%

|

24.42%

|

|

Earnings per share

|

6.75

|

7.78

|

7.48

|

–

|

|

Interest and investment income

|

–

|

–

|

–

|

–

|

|

Interest expense

|

–

|

–

|

–

|

–

|

|

Net interest expenses

|

–

|

–

|

–

|

–

|

|

Depreciation and amortization charges

|

–

|

–

|

–

|

–

|

|

EBITDA

|

–

|

–

|

–

|

–

|

|

Gain or loss from assets sale

|

–

|

–

|

–

|

–

|

Hi, I’m Ronak, a news writer covering the latest updates in automobiles, education, smartphones, and trending topics. I focus on delivering simple, clear, and timely news to keep readers informed about what’s happening around the world.